The Meeting of the Heads of Government/Vice Presidents of the Organization of Turkic States (OTS) convened in Baku on April 2, 2026 offers a revealing snapshot of a regional framework. What was once largely a symbolic platform built around shared historical, linguistic and cultural ties is now being revisioned to become a vehicle for economic coordination at the heart of Eurasia.

The Baku meeting did not introduce a radically new agenda, but it made one thing clearer than before: the OTS is beginning to measure its success less by declarations and more by its capacity to shape flows of trade, capital, and connectivity during the crisis periods of the world.

From Aggregate Potential to Functional Economic Space

The economic weight of the OTS is often underestimated. Member states represent a market of more than 180 million people and an economy exceeding 2,1 trillion dollars in size. Their combined trade turnover is close to 1,2 trillion dollars and the volume of exports between the members reached 40 billion dollars annually as shown in Table 1. This places the organization among the more trade-exposed regional clusters in the global economy. This outward orientation is driven by a mix of energy exports, manufacturing output, and growing industrial bases, particularly in Turkey and Uzbekistan, alongside resource-rich economies such as Kazakhstan, Turkmenistan and Azerbaijan.

| Category | Country | Population (Millions) | GDP (Nominal US$ Billion) | GDP per Capita (Current US$) |

| Member | Turkey | 88.6 | 1,358.0 | $15,325 |

| Member | Kazakhstan | 20.3 | 300.0 | $15,100 |

| Member | Uzbekistan | 37.7 | 137.5 | $3,514 |

| Member | Azerbaijan | 10.2 | 76.4 | $7,604 |

| Member | Kyrgyzstan | 7.2 | 20.2 | $2,747 |

| Observer | Hungary | 9.5 | 237.1 | $24,809 |

| Observer | Turkmenistan | 7.1 | 89.0 | $13,338 |

| Observer | Northern Cyprus (TRNC) | 0.5 | 7.1 | $15,835 |

| TOTAL | 8 States | ~181.1 | ~$2,225.3 | Avg. ~$12,285 |

| Table 1: Economic and Demographic Profile of the Organization of Turkic States (2025-2026) based on The Observatory of Economic Complexity. | ||||

Recent investment patterns indicate that this shift has already begun, albeit unevenly. Member’s multi-billion-dollar investments across member states, along with emerging joint financial instruments, point to a more use of capital as a tool of integration. At the same time, proposals for a common industrial platform suggest that OTS economies are starting to explore how to connect production systems rather than simply exchange finished goods. This matters because without integrated value chains, trade expansion will remain vulnerable to external shocks as happened in 2008 and 2014 crises.

The export structure of the bloc further reinforces the need for coordination. Energy exporters dominate in hydrocarbons, while manufacturing capabilities are concentrated in a limited number of economies. This creates both opportunity and risk. On the one hand, complementarities exist that could support deeper integration, particularly in energy-intensive industries. On the other, the absence of coordinated industrial policy risks perpetuating asymmetries and limiting the development of a balanced regional economy.

Connectivity, Energy Corridors, and the Strategic Logic of Integration

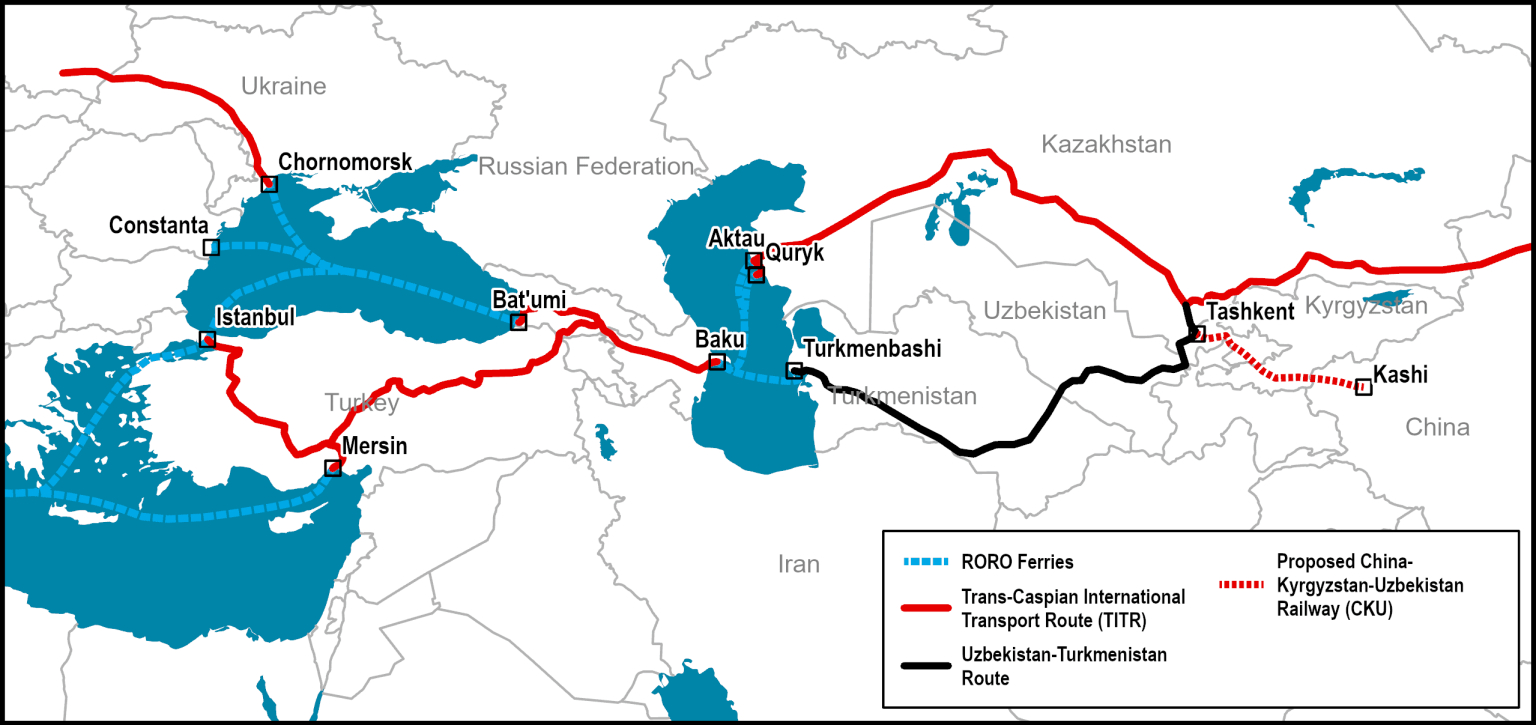

If economic integration is the objective, connectivity is the mechanism through which it can be realized. The OTS sits at the crossroads of Eurasia, and its geography gives it a structural advantage in shaping transcontinental trade. The Middle Corridor has emerged as the centerpiece of this strategy, offering a route that links China to Europe via Central Asia, the Caspian basin, and Turkey. In an era where traditional routes are increasingly politicized or congested, this Turkic Corridor represents both an economic opportunity and a geopolitical alternative.

{kind=link}

However, the viability of this route depends on a level of coordination that has not yet been fully achieved. A functioning corridor requires not only infrastructure investment but also synchronized policy frameworks across transit states. In this regard, the simultaneous integration of Kazakhstan and Turkmenistan into the operational logic of the corridor is essential. Treating these routes as parallel rather than interconnected limits efficiency and reduces the overall competitiveness of the corridor.

The Caspian Sea represents both a bridge and a bottleneck in this system. While maritime transport across the Caspian has improved, it remains insufficient to support large-scale, uninterrupted and unimpeded trade flows. This is where the long-discussed idea of a Trans-Caspian pipeline gains renewed relevance.

Beyond its energy implications, such a pipeline would symbolize a deeper level of infrastructural integration, linking Central Asian energy producers more directly to South Caucasus and European markets. It would also complement existing transport corridors by embedding energy flows within the broader connectivity architecture of the OTS.

The role of Azerbaijan in this equation is central. Its infrastructure investments, logistical capabilities, and geographic position make it the natural hub of the corridor. President Ilham Aliyev’s emphasis on completed and ongoing projects reflects a strategic effort to anchor regional connectivity around Baku. At the same time, initiatives such as the Zangezur route and the Kars-Nakhchivan railway indicate that connectivity is being approached not as isolated projects but as an integrated network.

Unlocking Turkmenistan: Energy Flows in the Turkic Corridor

A further dimension that deserves greater emphasis is the role of Turkmenistan in reshaping the energy and economic geography of the OTS space. Turkmenistan holds the world’s fourth-largest proven natural gas reserves, estimated at around 20 trillion cubic meters, yet its export structure remains highly concentrated.

In recent years, more than 70 percent of its gas exports have been directed to China via the Central Asia-China pipeline network. This level of dependency creates structural vulnerabilities, limiting Ashgabat’s bargaining power and exposing its economy to fluctuations in a single market.

The prospect of integrating Turkmen gas into westward energy corridors, particularly toward European markets, would therefore represent a significant strategic shift. For the OTS, this is not merely an energy issue but a question of systemic integration, as Turkmenistan’s fuller participation would add both volume and depth to the organization’s economic architecture.

From the European perspective, the timing is equally critical. As the European Union continues to diversify its energy suppliers in the wake of reduced dependence on Russia, interest in alternative sources from the Caspian basin has grown steadily. A trans-Caspian connection that would enable Turkmen gas to flow through Azerbaijan and onward via the Southern Gas Corridor could become a cornerstone of this diversification strategy.

Beyond immediate supply considerations, such a development would deepen economic and political ties between Turkmenistan and European markets, opening space for broader trade and investment engagement. At the same time, reducing overreliance on a single export destination would allow Turkmenistan to pursue a more balanced economic model.

The Turkmen side is eager to realize this perspective. In turn, a more economically diversified Turkmenistan would reinforce the resilience and strategic coherence of the broader Turkic Corridor, strengthening its position as a viable and competitive axis of Eurasian connectivity.

Connectivity Will Remain Core Element

What is emerging is a layered understanding of connectivity. It is no longer limited to transport infrastructure but extends to energy networks, digital systems, and regulatory alignment. This multidimensional approach increases the strategic value of the OTS but also raises the complexity of coordination. Without institutional mechanisms capable of managing this complexity, the risk of fragmentation remains high.

From a geopolitical perspective, the OTS is positioning itself as a facilitator of middle power coordination in a fragmented Eurasian landscape. Its members are not seeking to replace existing global structures but to complement them by creating alternative channels of cooperation. This is particularly evident in their approach to connectivity, which aims to diversify routes rather than monopolize them.

The Baku meeting ultimately highlights a critical juncture for the OTS. The organization now possesses many of the elements required to become a meaningful regional actor: a sizeable market, significant trade capacity, strategic geography, and a growing set of institutional tools.

What remains uncertain is whether these elements can be brought together into a coherent and functional system. If the OTS succeeds in aligning its economic ambitions with its connectivity strategies, it could emerge as a key node in Eurasian trade and energy networks.